DiFeng Composite Co.Ltd(Nanjing)

电话:86-025-57450287

86-025-57450153

传真:025-57450153

邮箱:nanjingdifeng@163.com

地址:Baima Industrial Park, Lishui District, Nanjing City, Jiangsu Province

Remarks: The research date is August 30, 2019, and is issued for your reference after authorization.

01

China's rare earth production dominates Shantou

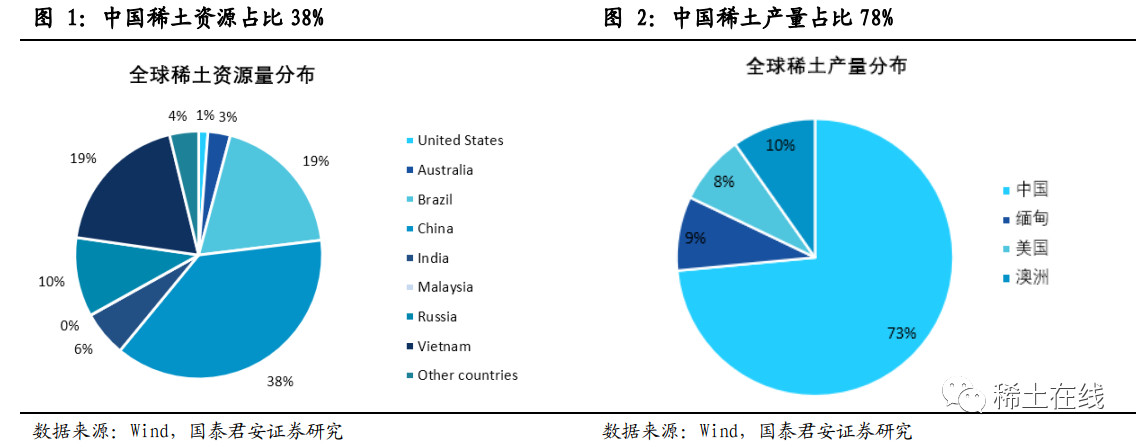

According to 2019 annual USGS rare reports, the world's proven rare earth resources amount to 1.2billion tons of global annual production of rare earths 18.5 Wandun REO estimates, the reserve-production ratio was 650 years, overall no shortage of rare earths. Global rare earth resources are distributed in China ( 38% ), the United States ( 19% ), Vietnam ( 19% ), and Russia ( 10% ).

China's rare earth production ranks first in the world. Excluding recycled waste (45,000 tons of REO), the annual global production of rare earths is 185,000 tons of REO, and China's output is 136,000 tons, accounting for 73%, contributing most of the world's production. Other supplies come from Australia's Lynas mine (10%), Myanmar mine (9%), and US MP (8%). China basically controls the supply of heavy rare earth ore. Since most of the heavy rare earth mines are concentrated in southern China and Southeast Asia, the supply of heavy rare earths is mainly from the heavy rare earth mines in southern China and the Myanmar mines. The Myanmar mines are basically selected and shipped to China for processing. Overall, Chinese companies Basically control the supply of heavy rare earth minerals around the world.

China's rare earths are heavy in the south and heavy rare earths are relatively scarce. The distribution of rare earth resources in China has always been said to be “Southern and North Light”. The abundant light rare earth resources are mainly distributed in the northern regions, including Baotou (Northern Rare Earth), Shandong, and Sichuan (Shenghe Resources), which mainly contain plutonium. The rare earth elements have very little strontium content; while the heavy rare earths are only distributed in the southern regions, mainly in Jiangxi Yinzhou (Five Minerals Rare Earth), Guangzhou (Guangzhou Nonferrous Metals), Guangxi, Fuzhou (Xiamen Tungsten Industry), and special heavy rare earth elements. Harmony, also contains 镨钕, 镧铈 basically no. Overall, the representative products of heavy rare earths are relatively scarce.

1.1. Overseas rare earth projects are difficult to advance and costly

China believes that there are very few rare earth mines running, only the Australian Lynas mine, the Myanmar mine, and the US MP . We take the most concerned Lynas rare earth mine overseas as an example to analyze the difficulty of overseas rare earth construction production lines.

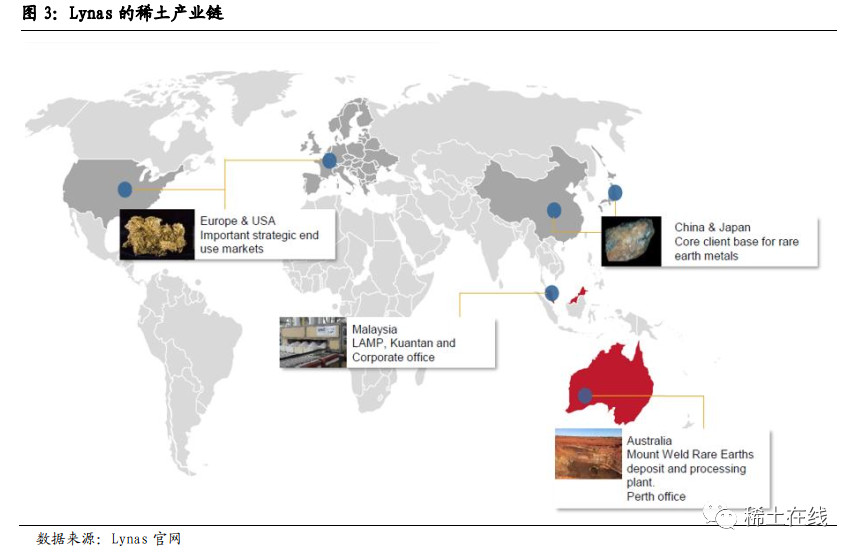

Lynas' main rare earth industry chain layout:

Rare earth mine: Mt Weld mine (light rare earth mine) in Western Australia , with a production capacity of 22,000 tons of REO . Rare earth smelting: Malaysia LAMP plant, supporting smelting capacity of 22,000 tons of REO . Rare earth sales: mainly sold to Japan, China, Europe and the United States, the largest supplier in the Japanese market .

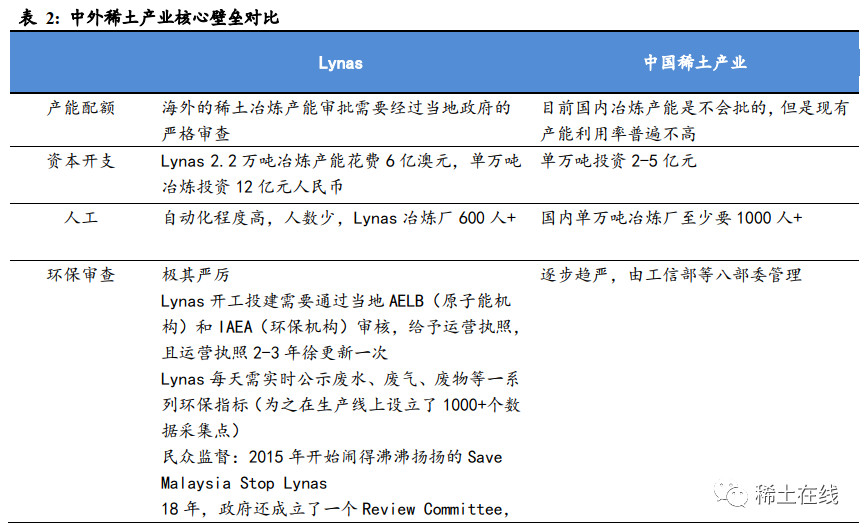

6 years of construction, 6 years of climbing, the process is long and difficult. Lynas plans to build a rare earth smelter in Malaysia in 2007. It was originally planned to be put into operation in 2009Q4. However, due to the Malaysian government's review and other issues, the project construction progress was much lower than expected. After several delays, it was only firstly put into production in 2012. Production, the first time in 2013 to produce rare earth products and sales, 3 years later than originally planned, can not be described as not difficult, also missed the 2010-2011 rare earth price rose 10 times the magnificent cycle.

After the production, it is still troublesome. 1 The Malaysian government's review continues. Lynas's construction and construction needs to be approved by the local AELB (IAEA) and IAEA (Environmental Protection Agency), and the operation license is granted. The operation license is updated 2-3 years. In 18 years, the government also established a Review Committee to assess the impact of Lynas on environmental health and safety. 2 Strict monitoring of environmental indicators, Lynas needs to publicize a series of environmental indicators such as wastewater, waste gas and waste in real time (for which 1000+ data collection points have been set up on the production line). 3 Public supervision and opposition of the people march: Malaysia, 2015 The public worried about environmental pollution and marched. The slogan at the time was “Save Malaysia Stop Lynas”.

The overseas rare earth industry chain has high investment costs, and China's rare earth smelting has core barriers. Regardless of the Capex perspective or the later operating costs, the cost of overseas Lynas investment is much higher than that of the domestic market. In the early stage of construction and post-operation, the overseas government has strict supervision on the rare earth industry chain and the public demand is extremely high. The industry chain will bear part of the cost of externalities. The overall achievement of the core competitiveness of China's rare earth smelting process.

02

Rare earth supply pattern gradually improved

2.1. Myanmar rare earth mine supply contraction

According to reports of rare earth Shui Road, 2018 Nian 11 Yue 3 date, the border between China and Myanmar in Yunnan Tengchong customs retreat, all the resources of Myanmar temporarily ban products by Tengchong customs import to China. Then in December , Tengchong Customs temporarily allowed the Myanmar Rare Earth to enter the customs, with a continuous switch date of 5 months. The switch is a temporary measure aimed at giving Myanmar's rare earth miners (mostly Chinese citizens) and enterprises a buffer period to reduce losses, so that they can handle existing stocks and even deal with fixed assets such as equipment. In May 2019 , Tengchong Customs officially suspended the import of rare earth resources in Myanmar.China's rare earth imports fell sharply in June 2019 .

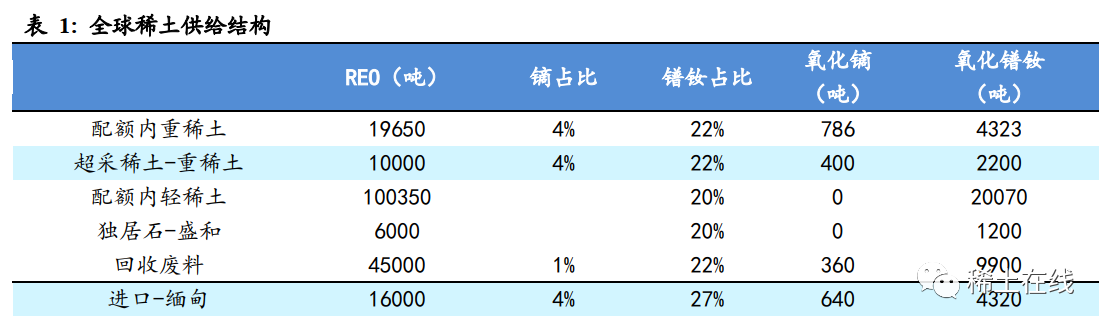

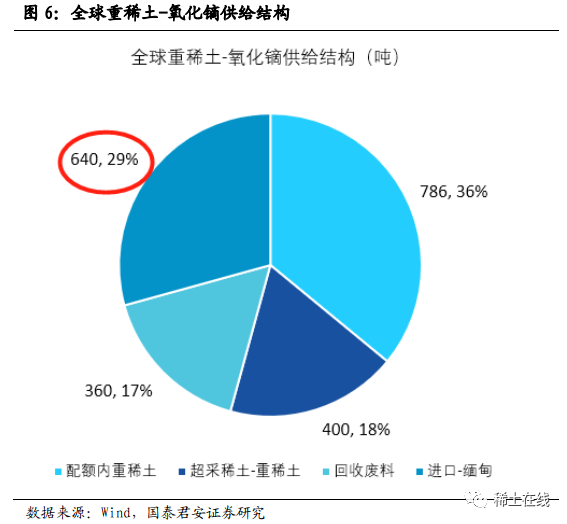

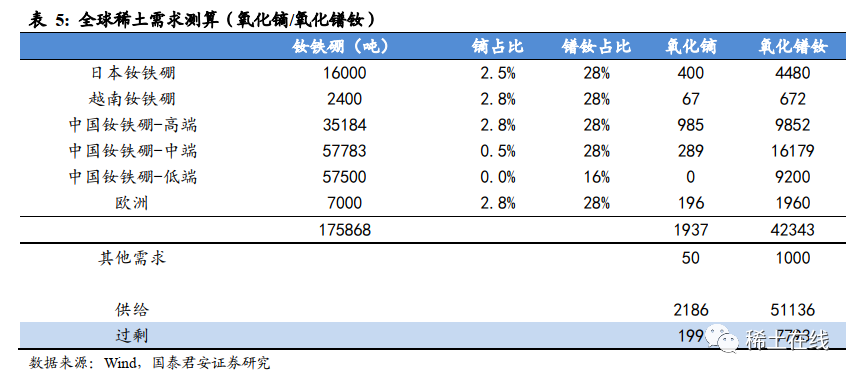

Rare earths in Myanmar ban or directly affect the supply of nearly 30% of heavy rare earth cerium oxide. We forecast a total of 2,186 tons of global cerium oxide supply in 2018, China contributed 71% of production, and the remaining 29% came from Myanmar. Of the 120,000 tons of China's compliance rare earth quotas, only 20,000 tons are less than ionic heavy rare earths, and more than 100,000 tons are light rare earths. The heavy rare earths in the quotas produce about 786 tons of cerium oxide, accounting for 36%; In addition, we assume that there is still a small amount of super-harvested rare earths, and it is expected to produce 400 tons of cerium oxide. Waste recycling yielded 360 tons of antimony oxide, accounting for 17%. On the whole, the supply of heavy rare earths is very concentrated, and Myanmar accounts for nearly 30% of the supply, which is very important.

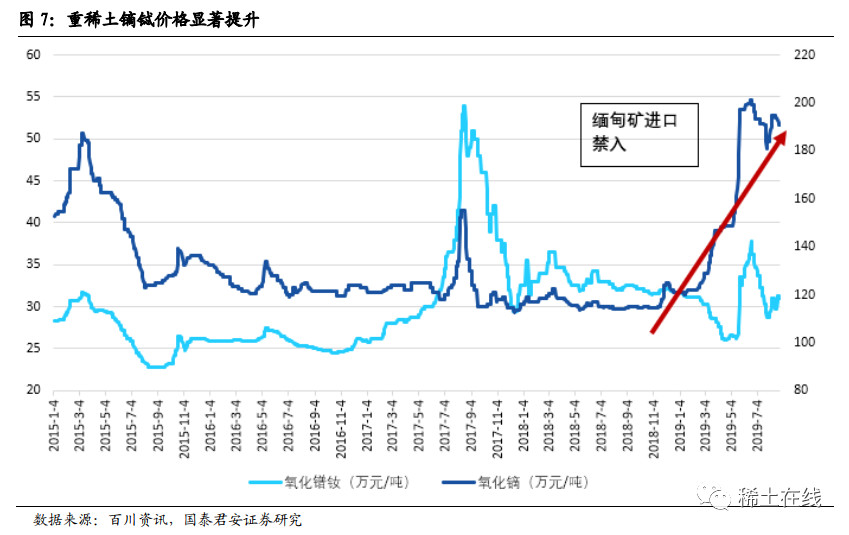

Affected by this influence, the price of antimony oxide rose by 65% from the bottom of 1.15 million/ton to the current 1.9 million/ton. We believe that the price of heavy rare earth lanthanum oxide will remain high in the future.

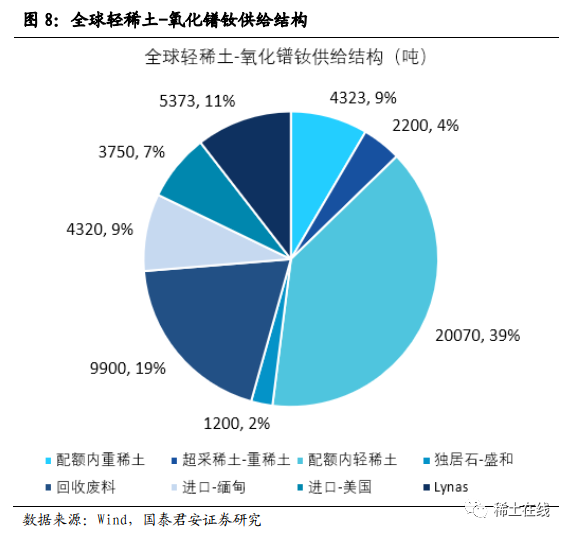

The ban on rare earths in Myanmar also improves the supply pattern of light rare earths. We predict that the global supply of antimony oxide will total 51,000 tons in 2018, China contributes 73% of the output, and overseas supply accounts for 27%, of which Myanmar accounts for about 9% of global supply. After the rare earth in Myanmar is banned, the supply of light rare earth antimony oxide It is also expected to shrink further.

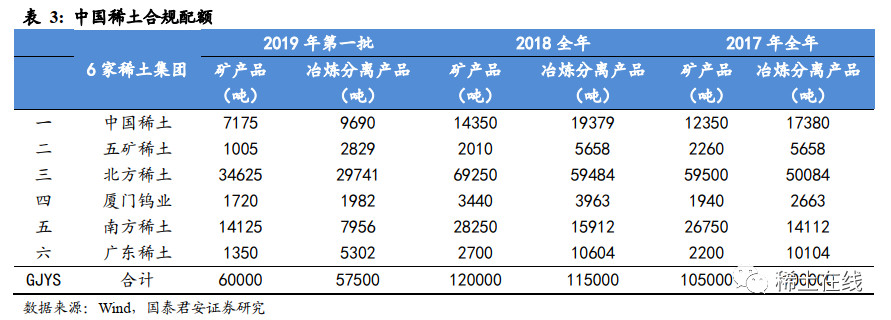

2.2. Six major rare earth groups + rare earth quota system management, industry compliance increment is limited

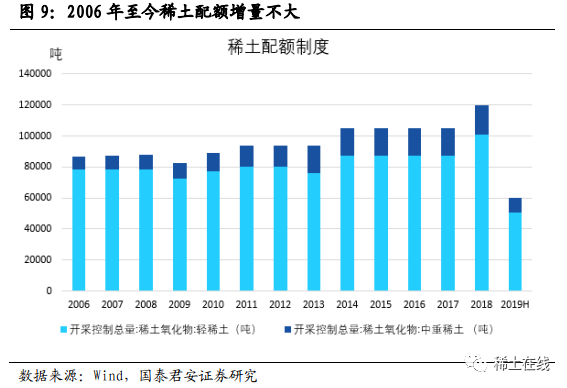

The supply side of China's rare earth industry is controlled by the quota system. In order to limit the blind development of the rare earth industry and regulate market behavior, the State Council’s Notice on Comprehensively Rectifying and Regulating the Order of Mineral Resources Development began in 2006.China’s rare earth industry began to implement the quota system, which is part of the Ministry of Industry and Information Technology and Natural Resources. The two batches allocated production quotas for rare earth mineral products and smelting and separating products in the first half of the year to the six major rare earth groups. It is required that the six major Rare Earth Groups strictly control the total amount of mining and smelting and separation, and no unit or individual may produce without plan or super plan. Since 2006, the increase in rare earth quotas has been small, with an annual increase of 2.8%. The Ministry of Industry and Information Technology and the Ministry of Land and Resources considered the downstream demand of rare earths as a consideration, and issued quotas. In 2006 , the first batch of rare earth mining quotas was 86,500 tons. Then, according to the downstream demand, whether the adjustment is increased or not , the annual rare earth mining quota for 2018 is 120,000 tons. The 12- year quota compound annual growth rate is only 2.8% , and the overall industry compliance effective supply growth rate is not large.

In 2019, the first batch of mineral products quota was 60,000 tons, which is half of that in 2018. It is estimated that the overall mineral product quota in 2019 will be flat in 2018, which is 120,000 tons. We believe that the rare earth quota system has laid a solid foundation for the healthy development of the overall rare earth industry.

2.3. Domestic rare earth industry continued to improve, and the pattern of rare earth industry continued to optimize

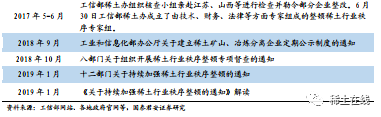

The rectification of the rare earth industry and environmental protection continued to advance, and the pattern of the rare earth industry continued to be optimized. As a large country of rare earth production, the country releases annual production quotas for rare earths to control the overall supply situation. The rare earth mining and over-exploitation have always been the biggest reason for the supply of rare earths. We found that with the normalization and institutionalization of the domestic rare earth industry in 2017, the ills of the rare earth industry have gradually improved and eliminated, and the pattern of the rare earth industry has continued to be optimized. After 2017, in the normalization of the rare earth industry, unlike the previous thunder and heavy rain, it has begun to take its place. The inspector team went to various factories to check and ordered the production to stop. At the same time, the management and control of the six major groups in the past is relatively weak. The mining/smelting directives of the six major groups are truly on the ground, and with the continuous advancement of environmental protection, the “black rare earth”, a highly polluting over-exploitation supply contain.

03

The demand for magnetic materials is gradually recovering, and the prospects for light and heavy rare metals are clear.

The downstream demand for rare earth magnetic materials has gradually recovered. Rare earth lanthanum and lanthanum are mainly used in NdFeB magnets. The downstream of NdFeB magnetic materials is mainly used in wind power, inverter air conditioners, automobiles (especially new energy vehicles), and industrial robot motors. In terms of automobiles, global new energy vehicles have exploded in recent years, and the increase in automotive microelectronics applications has increased the demand for servo motors. The demand for high-end NdFeB has rapidly increased. In terms of home appliances, after 19 years, the new version of home appliances stimulated consumption, the promotion of smart green appliances, the gradual penetration of inverter air conditioners will also enhance the use of NdFeB. In addition, the wind power curtailment phenomenon in the domestic wind power industry has gradually improved. The industry recovery drives the growth of the wind turbine business and the rapid development of industrial robots can all drive the continuous growth of demand for NdFeB. Light and heavy rare earth supply and demand have improved, and the prospects are clear. With the rectification of the national rare earth industry, we found that the supply demand for cerium oxide has basically returned to a more balanced state, with a surplus of about 9% . If 29% of Myanmar 's supply is affected, then strontium oxide will be in short supply and prices will continue to rise. In terms of antimony oxide, the supply is relatively loose, and the supply is about 15% . If the supply of 9% bismuth oxide inMyanmar is limited, the overall supply pattern of light rare earth will also be optimized.

扫一扫